Author: Carlos Salas Najera

The dominant role of big technology firms since the GFC (Global Financial Crisis) cannot be understated with their market capitalization dwarfing "traditional economy" stocks. One of the factors behind the demise of "value" as an investment style during the last decade has been the lack of tools available for investment professionals to properly identify and factor intangible assets into their models. In this way, the use of alternative data focused on patent and IP valuation will be increasingly important going forward for the investment management industry.

In this first article, an introduction will be provided about past research papers focused on accounting-related intangible items, and their implications in terms of absolute and risk-adjusted returns for investors with emphasis on equity strategies. A future article will provide more results about the role of alternative data and machine learning as an evolutionary step to factor intangibles into a data-driven investment process. In the meantime, the reader can also find more information about these two areas in a recent webinar organized by the CFA Data Science WG.

The Intangibility Importance in the 21st Century Investments Industry

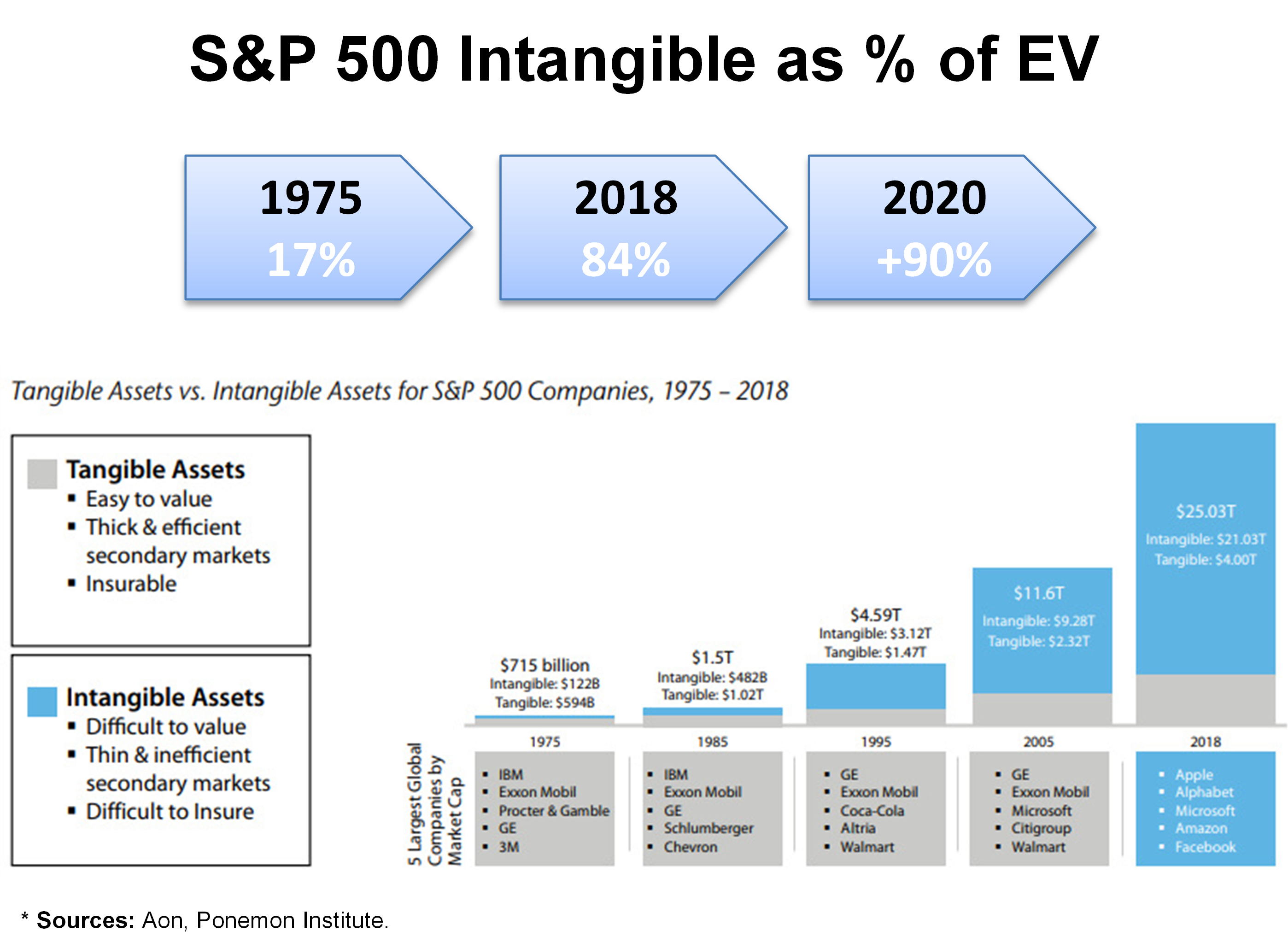

The composition of the asset mix of the average company in the S&P 500 was clearly made out of physical assets. In this way, the average company in the S&P 500 had less than 20% of its enterprise value in intangible assets in 1975. With the advent of the 21st century digital era and the fourth industrial revolution, this percentage of the intangible mix has been increasing at a staggering pace and is more than 85% of the enterprise value as of 2020 (source: Aon, Ponemon Institute).

The value of U.S. intangible assets is estimated at around $20-$25 trillion dollars 2020 (source: Aon, Ponemon Institute) with items such as e-commerce platforms, digital assets and other “soft assets” (e.g. brand reputation) more than surpassing in terms of importance traditional assets such as PP&E (Property, Plant and Equipment), and becoming a real challenge for those agents in charge of conducting financial valuation of a company such as equity analysts, investment bankers, or auditors.

In this context, those investors still anchored in the past using traditional valuation techniques that underestimate or ignore the role of intangibles are destined to fail. New valuation techniques based on ML (Machine Learning) and the use of accounting and alternative data to value the intangible assets of a company, are to play a more important role in the future.

Intangible Research based on Accounting Items

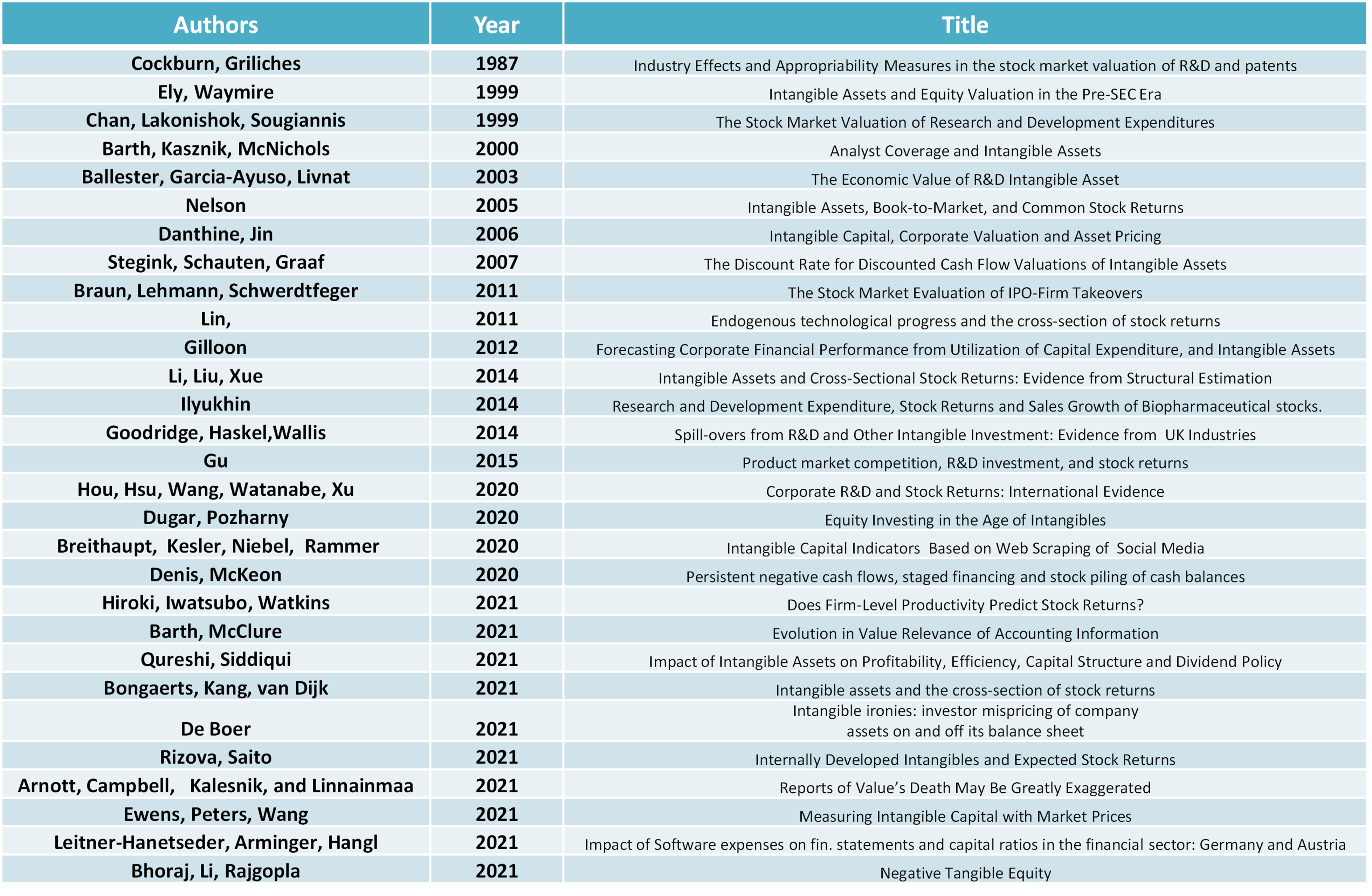

The table below contains a comprehensive summary of research papers published over the last four decades that use mainly accounting-based intangible data in order to study how the level of intangible intensity impacts multiple corporate facets such as cross-sectional stock returns predictability, M&A deals success, or cost of capital estimation; among many others. Most of these papers are freely available online using sources such as ssrn.com.

A thorough review of these research papers unveils important insights about the role of intangibles.

Intangibility valuation is challenging

Patent information and accounting items are useful tools to explain valuations but both have limits: patent information is subject to significant estimation error and accounting items lack detail preventing the appraisal of the actual value of a company’s intangible asset base without significant suffering from an acute risk of estimation.

Machine Learning models to the rescue

Stochastic ML (Machine Learning) models deliver better results than deterministic methods when estimating the market value of an intangible asset.

The intangible factor matters especially for Growth stocks

R&D (Research and Development) and subsequent intangible recognition are especially relevant when conducting cross-sectional analysis of growth stocks.

Significant Interplay between intangibility and CapEx (Capital Expenditure) intensity efficacy

Firms with a high intangible mix in their asset base generate superior value-added from their future CapEx investments than those firms with low intangible intensity.

Intangibility lures investor interest

Price discovery fostered by analyst coverage is linked to intangible intensity.

The link between intangible risk and cost of capital

The cost of capital of an intangible asset is extremely difficult to evaluate but has been estimated to be higher than a company’s WACC (weighted-average cost of capital) with several researchers finding that cost of equity can probably act as the better proxy.

Separate the chaff from the wheat

Goodwill is non-organically generated balance sheet item born from non-organic activity i.e. mergers and acquisitions (M&A). Regrettably, M&A deals have historically destroyed value due to M&A integration challenges and deal overvaluation risk. Therefore, the goodwill component must be expunged from the total intangible asset item of the balance sheet in order to filter a relevant accounting-based metric that only accounts for organically-generated intangible items e.g. patents, IPR, etc.

M&A arbitrage considerations

Regarding the previously mentioned failure of M&A deals to create shareholder value, it would be worth pointing out that the more successful deals ex-post are those involving a target company with a high intangible mix, an already finished product, and low or no founder risk.

Do not believe the R&D-to-Sales Hype

Contrary to popular belief, intangible intensity has been found to be measured more optimally using fundamental ratios like “R&D-to-Market-Cap” and “R&D-to-Enterprise-Value”; whereas the popular “R&D-to-Sales” ratio has been less effective due to the higher volatility of the denominator.

The higher the intangibility potential, the higher the productivity

The relationship between R&D and future TFP (Total Factor Productivity) is statistically significant in many companies across multiple geographies i.e. companies allocating more budget to R&D activities are more likely to eventually recognize an intangible and benefit from superior productivity levels.

Do not play down the degree of competition

An intangible factor created using accounting items is particularly significant predicting cross-section stock returns of firms active in more competitive industries (low industry concentration), than for those experiencing oligopolistic or duopolistic status.

Intangibility is part of the “risk premia” family

Authors found that the intangible premium does seem to be associated with higher risk features such as higher stock volatility or increasing perception of default risk. In other words, the intangible factor efficacy does not seem to be a market mispricing that could be associated to a failure of the perfect competitive hypothesis of the markets.

Higher intangible intensity is not a silver bullet

As mentioned in the prior paragraph, intangible premium is synonym of higher risk and, as a consequence, some authors highlight that significant shareholder dilution has been experienced by firms with high intangible intensity and persistent higher-than-average cash balances suffering from a consistent negative net cash flow generation.

The intangible factor is statistically significant

Multiple authors have found that multiple strategies using multiple ways of creating intangible-driven portfolios (e.g. long high intangible and short low intangible) result in significant absolute and risk-adjusted returns that survived multiple performance attribution models such as Fama-French’s 5 Factor model.

Intangible as a standalone or add-on strategy

Recent findings show that value-driven strategies can be enhanced by adjusting book value using intangibles and SG&A information. Nevertheless, other authors recommend to use intangible screening criteria in order to preserve the purity of the value factor.

Alternative data to play a bigger and complementary role to intangible accounting items

Accounting-related Intangible items have been reported by several authors to start suffering from alpha decay. As investors are able to access research more easily, the intangible factor has become more ubiquitous and easier to arbitrage than in the previous decades. As a result, investment managers are in the hunt for non-conventional alternative data beyond accounting items in order to enhance their models.

Conclusion

Intangibility is becoming an important part of the valuation puzzle and even the risk management process of an investment strategy. The body of research of the last three decades has delivered interesting insights about the importance of intangible-related accounting items; yet the advent of machine learning techniques and new alternative datasets promise to unveil new alpha-generating discoveries henceforth. The reader can find more information about these two areas in a recent webinar organized by the CFA Data Science WG and a new article to be released in the future.