Asset-Based Lending (ABL): A powerful tool for mid-market value creation

Author: Joe K. Wood

On 25 March 2026, the CFA UK Private Markets Community hosted its first in-person event, which was held at Wells Fargo’s offices in the City of London. The evening brought together over 140 attendees, spanning private equity sponsors, credit fund managers, debt advisors, asset valuers, and other institutional investors, for a panel discussion on asset-based lending and its role in mid-market value creation.

Private credit is under scrutiny of late. Major funds are gating redemptions. Alleged collateral fraud has exposed due diligence gaps across the lending chain. And a decade of financial engineering in asset-light, high-growth sectors is meeting reality as AI disrupts the portfolios that direct lenders built their books around.

Against that backdrop, the CFA UK Private Markets Community held its inaugural event at Wells Fargo in London, bringing together practitioners from across the mid-market ABL ecosystem to examine a product that, despite decades of proven performance, remains underutilised in European capital structures, and to ask a specific question: how does ABL create value for private equity sponsors?

The panel, moderated by Tom Weedall, EMEA Head of Commercial Bank and WFCF UK, Wells Fargo, featured

- Marc Finer, Principal, Debt Financing and Capital Markets, Aurelius

- Jake Hyman, Managing Director, Blazehill Capital

- Lisa Montgomery, Gordon Brothers

- and Chris Hall, Executive Director, Hilco Global Professional Services

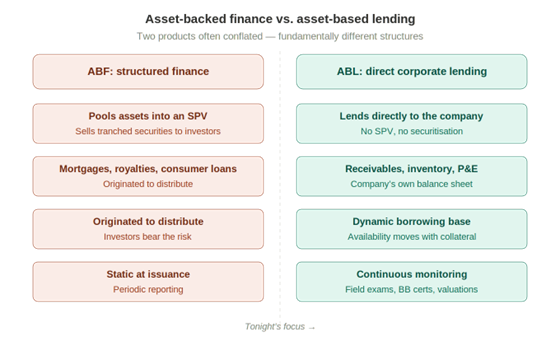

First, a Distinction That Matters

Asset-based lending and asset-backed finance are not the same product.

Asset-backed finance (ABF) is structured finance: pooling cash-flow-producing assets into a special purpose vehicle and selling tranched securities against them. ABF encompasses everything from residential mortgages and credit card receivables to aircraft leases and entertainment royalties. Its structural protections (bankruptcy-remote SPVs, diversified collateral pools, and hard-wired cash flow waterfalls) have historically produced lower default rates than corporate credit across multiple market cycles.

Asset-based lending (ABL) is a form of corporate lending. The lender lends to the company itself, secured against the company’s own balance sheet (receivables, inventory, plant and equipment, freehold property and even some intellectual property) with no SPV and no securitisation. The borrowing base moves dynamically with the collateral, monitored through field exams, borrowing base certificates, and independent valuations.

The distinction matters because the two products carry fundamentally different risk profiles, recovery mechanisms, and structural protections. Conflating them, as the market often does, obscures the strengths of each.

The Value Creation Case for Private Equity

The panel’s answer to the central question came from multiple angles but converged on a clear thesis: ABL creates value for sponsors not by being a cheaper version of cash flow lending, but by financing situations that cash flow lending structurally cannot reach.

The starting point is how each product underwrites. Cash flow lending is based on historical EBITDA and requires a clean, backwards-looking story to offer competitive terms. For carve-outs, where standalone financials may be weak, non-existent, or distorted by the separation, that story often does not exist. ABL, as Finer put it, is “much more sympathetic to the past, because it’s looking at what the assets are now.” It constructs a facility around the balance sheet as it stands today, not around a historical earnings trajectory.

The result is fourfold:

- First, sponsors can finance transactions that would otherwise require significantly more equity

- Second, the cost of capital is materially lower — senior ABL facilities were cited at 2–4% over base, well inside conventional leveraged finance

- Third, the covenant package is lighter, giving management teams operational room to execute the turnaround or improvement plan without tripping financial tests during the transition period

- And fourth, because a senior ABL revolving facility moves with working capital, availability scales with the business

The panel also noted that the product can serve as a growth tool, providing an efficient and fast route to financing bolt-on acquisitions for sponsors building platforms.

A further practical dimension emerged from the deal execution side. The real opportunity lies in threading the needle between the two mindsets: combining an ABL revolver against working capital at low cost with a cash-flow term loan that provides quantum certainty earlier in the process. That blended structure can deliver more total debt capacity than either product alone, at a lower weighted cost, with greater flexibility.

Collateral Is Only as Good as Its Liquidity

The discussion was grounded in recovery realities. Net book value, the panel argued, has nothing to do with likely debt capacity. A fixed asset register filled with software and leasehold improvements tells a lender nothing. What matters is the liquidity analysis around those assets: who the buyers are likely to be, and where they will be.

The panel explored this through a live example: an aircraft parts business jointly funded by a senior and a junior lender, where specialist inventory requires fundamentally different liquidation assumptions than retail stock. A junior lender’s willingness to underwrite an 18-month liquidation where a senior lender prices at 12 months is what generates incremental availability for the borrower, but only where the underlying asset intelligence supports it.

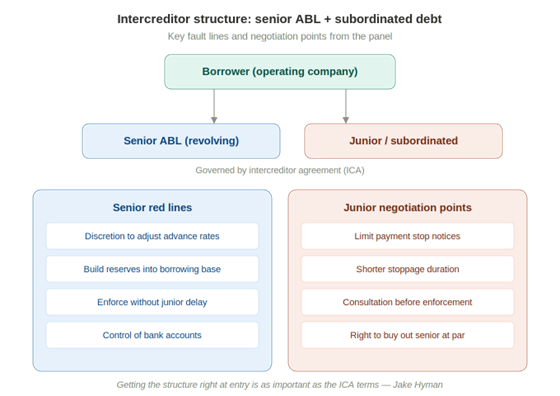

Structuring Senior and Junior: The Intercreditor in Practice

Where a capital structure layers senior ABL with subordinated debt, the intercreditor agreement governs how the two lenders coexist, and the panel was candid that this is where complexity lives.

The key fault lines were clearly drawn. Senior lenders will not compromise on their ability to adjust advance rates or build reserves to protect their collateral position, and will resist any consultation obligation with the junior that might delay enforcement and impair recoveries. For the junior lender, the negotiation centres on limiting payment stop notices and preserving the right to buy out the senior’s position at par if the junior believes the business can be turned around.

Getting the structure right at the point of entry, with enough liquidity and aligned exit strategies, is as important as the intercreditor terms themselves.

Direct Lending’s Structural Blind Spot

There is a direct line between sector exposure and portfolio resilience. Direct lending followed sponsors into asset-light, high-growth sectors (software, healthcare, TMT) and those portfolios now sit exposed to AI-driven valuation compression with no physical collateral underneath. ABL portfolios, concentrated in the “old world economy,” have physical assets providing a recovery floor regardless of earnings volatility.

The structural point was reinforced from a lender’s perspective. ABL may be financially covenant-lite, but the monitoring infrastructure (monthly borrowing bases, quarterly field exams, control of borrower bank accounts, spot checks on receivables) provides surveillance depth that most direct lending structures do not replicate. Where direct lenders have relaxed ABL principles to compete on speed and flexibility, the consequences are now becoming visible.

The same point came through from the borrower’s perspective: stress situations with cash flow lenders tend to create more friction than with ABL lenders. The probability of default may be present, the panel argued, but the loss given default should always be very low or zero, because the model is backed by collateral.

Market Depth and What’s Next

The US ABL market accounts for roughly 30% of all corporate lending. In the UK, the figure sits closer to 5–10%. But the trajectory is clear: a decade ago, a £60 million UK ABL facility required three lenders; today, a single lender can comfortably hold £100 million, and a small handful of banks can support facilities of £300–400 million.

The panel’s consensus was that ABL remains structurally underutilised in European PE portfolios, held back less by its economics than by familiarity.

JOIN OUR PRIVATE MARKETS COMMUNITY

We’re connecting the minds shaping private capital in a brand-new community. CFA UK’s Private Markets Community is dynamic, collaborative, and open to all interested in the emerging world of private markets and investments. Combining exclusive events with expert insights, and bringing you closer to new colleagues and friends, this is the place to go to stay on top of what’s happening in private capital.

FIND YOUR COMMUNITY

Related Articles