Top financial scandals and lessons for investors and analysts - Part 3

Author: Andrew Haskins, ASIP

Listed developers in the Chinese residential property crisis (c.2020 onwards): beware the obvious flaw in the underlying business model

The Chinese residential real estate market is now in the fifth year of a severe, slow-motion crisis or crash. Key housing metrics – unit sales, prices, construction starts and completions – are still sliding, while an estimated 80 million unsold or vacant homes clog the market. Numerous large residential developers have collapsed or defaulted on debt payments, while many more medium-sized or small construction firms across China are unable to service their debts or maintain normal operations.1

While the market started turning down in 2021, signs of impending problems had been visible for many years before. There has been much excellent research into the causes of the slump (notably, massive overbuilding in mid and lower-tier Chinese cities), and the implications for the national economy of the continuing crisis in the construction industry, which once made up one-quarter of Chinese GDP.

I followed the Chinese property crisis closely from two perspectives.

- Firstly, over 2013-2014 I worked in Hong Kong as executive director of equity research for a boutique firm called Asianomics, where among other sectors I focused on Chinese developers.

- Secondly, from 2016 to 2023 and again based in Hong Kong, I worked in physical property as head of Asia research for a global real estate services firm and then as head of APAC real estate investment strategy for a large fund manager.

The Chinese property crisis: a sharp rise, a sharper fall

In this article, I will focus on the impact of the Chinese property crisis on equity investors in the formerly high-flying listed residential developers. From the viewpoint of most investors, the crisis culminated in the collapse or near-collapse of several large and well-known developers listed on the Hong Kong Stock Exchange (HKSE), including Evergrande, China Vanke and Country Garden:

- The infamous Evergrande was once China’s top developer by sales, with a peak market value of US$52billion in 2017, but it was the world’s most indebted developer with over US$300 billion in debt when delisted from the HKSE in August 2025.2

- China Vanke, which became the first state-backed developer to request a delay on bond payments in late 2025, has seen its share price fall 88% in five years.3

- Country Garden, which defaulted on coupon payments on US$14 billion of overseas debt in late 2023, has seen its share price fall 97% in five years, though it has reached agreement with creditors and still operates.4

Strictly speaking, the Chinese residential property crisis should not be called a fraud or a scandal, since relatively few residential developers faced direct questions about financial propriety. Fraud was involved in the case of Evergrande, whose founder Hui Ka Yan pleaded guilty in April 2026 to charges including embezzlement of assets and corporate bribery after a trial in the city of Shenzhen.5

However, it is undeniable that the Chinese property crisis has resulted in large-scale value destruction for equity and debt investors in the Chinese residential property sector. It has almost certainly resulted in even greater value destruction for the tens of millions of Chinese households which invested in the physical apartments and houses that the developers built.

The fatal flaw: counting chickens before they hatch

The reason for including the crisis in a series of articles on the simplicity of many financial frauds is that there was a glaring flaw in the business model of some of the largest developers.

This flaw was reckless over-investment coupled with heavy reliance on pre-sales, i.e., sales before building completion. Gross mismanagement is not the same as outright fraud, but at some point the two sins start to merge.

It was not difficult to identify this flaw from the developers’ accounts. I did so – in two detailed equity research reports on the Chinese property development sector published in April and June 2014.

Both reports identified Evergrande as the developer at greatest risk, while the second highlighted the sector’s huge free cash outflows and pointed to Country Garden as a company for which risk was rising. This research was published at least six years before the crisis in the sector really broke.

Source: Asianomics research (June 2014)

Many other equity analysts identified severe weaknesses in the Chinese residential property developers long before the market peaked, so I did not possess unique foresight.

However, it is instructive to explore the key finding of my research at Asianomics. This was that the sector in aggregate was generating massive cash outflows despite a huge boost to cash flow from pre-sales.

How over-investment hammered an important economic sector

Selling housing units before completion is not intrinsically wrong. Indeed, it is quite a common practice in real estate, especially for luxury developments. However, as the Chinese experience was to illustrate, a business model built around heavy pre-sales of properties implicitly carries two risky assumptions:

- Property prices will always go up

- The property developer will stay solvent to complete the project

If property prices do not always go up, there is less incentive for buyers to pay for new residential units in advance. And if the developer does not stay solvent, there will be no completed units for any buyers to invest in. This second point is a greater risk for buyers than developers.

To be specific, the more aggressive developers pursued a strategy that involved both heavy buying of land reserves and rapid expansion of properties under development (i.e., new projects). In accounting terms, buying new land counts as capital expenditure, while expanding properties under development counts as additions to working capital. However, the combined result was huge aggregate investment.

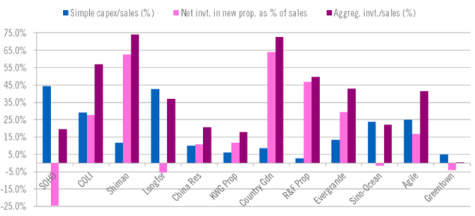

The figure below shows “aggregate investment”, i.e., reported capex combined with net additions to properties under development, for 12 large Chinese developers in 2013. Reported capex for the 12 stocks ranged from 3% to 44% of revenues.

However, three companies invested more than 45% of revenues in net additions to properties under development. As a result, aggregate investment reached 73-74% of revenues for Shimao and Country Garden, and the combined level for all 12 stocks was 43%.

Chinese property developers: aggregate investment as a proportion of revenues (2013)

Source: company accounts, Asianomics research (June 2014)

A chaotic – and predictable - collapse

Naturally, it is easier for a company to justify heavy investment if it generates high profit margins. In 2013, Evergrande stood out in the sector for recording aggregate investment of nearly 45% of sales despite achieving one of the lowest EBITDA margins, at just 21% compared to the combined sector level of 26% and a level closer to 30% for better-managed developers like China Overseas Land (COLI).

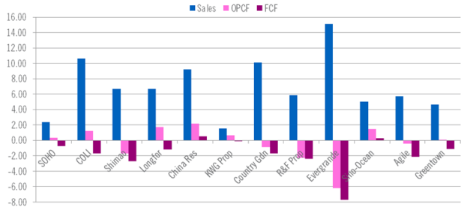

Consequently, Evergrande recorded the greatest free cash outflow in the sector in 2013, at RMB48.0bn (US$7.72bn at the exchange rate at the time) – equivalent to an extraordinary 51% of sales and 88% of tangible fixed assets.

In fact, Evergrande accounted for 37% of the aggregate free cash outflow of US$21.0bn for the 12 large developers in the sample in that year.

Chinese property developers: revenues, operating cash flow and free cash flow (2013)

Source: company accounts, Asianomics research (June 2014)

At the time, gearing and solvency metrics such as net debt/EBITDA and EBITDA interest cover for Evergrande were already among the poorest in the sector. Given the company’s predisposition to aggressive investment, it was not hard to predict that its financial position would deteriorate further.

It was also noticeable that Evergrande was a major issuer of “perpetual capital securities” – a form of hybrid financing treated on balance sheets as equity but with certain characteristics of debt.

To offset their huge aggregate investment spending, certain developers relied heavily on pre-sales of properties. In 2013, the most extreme case was Country Garden, which reported a free cash outflow of RMB10.5bn (US$1.74bn) despite a massive boost to cash flow of RMB30.1bn (US$4.85bn) from “advanced proceeds received from customers”, i.e., pre-sales.

Pre-sales increase cash on the asset side of a developer’s balance sheet, but produce a corresponding liability because the company has an obligation to deliver a completed housing unit to the customer.

Prepayments were so high for Country Garden that that they represented 31% of its balance sheet total at the end of 2013. However, Longfor, China Resources and Sino-Ocean were not far behind.6

How a fatal flaw stayed ignored

Why have we spent so much time discussing the Chinese residential property sector as it looked in 2014? To make the point again, we have done so to prove that the weaknesses of many large developers were readily identifiable years ahead of the property market crash.

The fundamental weakness was a reckless business model, but this was reflected in obvious issues in the developers’ accounts: over-investment, heavy free cash outflows, high liabilities to customers in the form of prepayments…. this picture was clear throughout the time that consistent price growth and strong volume growth resulting from aggressive expansion were driving headline sales.

It was also possible to point to Evergrande as the riskiest developer in the sector. This is the only large developer which both went into liquidation and admitted financial fraud. However, several other large developers pursued risky strategies that have left them under serious pressure and struggling to meet their obligations. Severe mismanagement is the underlying failing in this saga.

In this article, I have intentionally focused on financial analysis of the listed residential developers. My later experience in physical real estate research and investment strategy in Asia made the flaws in the Chinese developers’ strategies even more obvious.

From an investment perspective, the most attractive markets for residential projects in China were always the Tier 1 cities (Beijing, Shanghai, Shenzhen, Guangzhou) and leading Tier 2 cities. In contrast, many developers expanded aggressively into lower-tier cities with lower income levels.

In addition, by 2020-2021 new apartments in China’s Tier 1 cities had become highly unaffordable on standard affordability metrics such as price/household disposable income. Indeed, they ranked towards the top of the list of global gateway cities on this measure.7

A major correction in the Chinese residential property market therefore looked long overdue, and it has duly happened. An end to the housing slump is not yet clearly in sight, and the weak state of the property market remains a drag on the Chinese economy overall despite its many strengths and the high growth that China is already achieving in new areas like electric vehicles and AI.

To conclude, the key lesson for investors from Chinese residential property crash is to beware any clearly identifiable flaws in the underlying business model for a company or sector.

Such flaws are often easiest to spot by analysing the sector as a whole. Any companies with financial metrics that are clear outliers compared to the whole sector should be treated with great caution.

1 For a good, concise introduction to the overall crisis, see article China’s property slump deepens—and threatens more than the housing sector by Jeremy Mark for Atlantic Council’s GeoEconomics Center (28 January, 2026).

2 Evergrande’s $50 billion rise and fall leaves scars on China’s property sector, CNBC (25 August, 2025)

3 China Vanke’s bonds plunge on fears of waning state support, Financial Times (27 November, 2025). Share price decline as of 8 May, 2026

4 Country Garden Secures Backing For $14.1B Offshore Debt Overhaul, Mingtiandi (19 August, 2025). Share price decline as of 8 May, 2026

5 Founder of China's Evergrande pleads guilty to fraud, BBC News (14 April, 2026)

6 Source: company accounts, Asianomics research (June 2014)

7 See, e.g., Do High Residential Prices and the Evergrande Episode Signal Falling China Property Values? (Colliers International blog article, 7 October, 2021).

ABOUT THE AUTHOR

Andrew Haskins has over 35 years of financial experience across multiple markets and sectors. He spent 25 years as a senior equity analyst or head of equity research for investment banks including HSBC, Nomura and MUFG based in London, Paris, Tokyo, Riyadh and Hong Kong. Thereafter, Andrew moved into private real estate, spending eight more years in Hong Kong as head of Asia research for Colliers International and head of APAC real estate strategy for Schroders Capital. He then returned to the UK and worked for two years in corporate finance.

A holder of the ASIP designation, Andrew has twice been a Responsible Officer under the rules of the Hong Kong Securities and Futures Commission. A strong presenter and prolific writer, he is proficient in French and Japanese, and holds BA and MA degrees in Law and Japanese Studies from Cambridge University.